.jpg)

Invest about 15-minutes to gain a comprehensive understanding of Constrained Investor. Watch the movie

"We are a constrained nation full of Constrained Investors."

"We are a constrained nation full of Constrained Investors."

"We are a constrained nation full of Constrained Investors."

"We are a constrained nation full of Constrained Investors."

.png)

Better

Retirement.

"For insurance producers and insurers, Constrained Investor unlocks an opportunity that is as significant as it is unexpected."

.png)

Constrained Investor upends the longstanding business of retirement income planning. It introduces a completely new client segmentation framework that redefines how retirees' needs are assessed and served. Annuities are the indispensable, key component of a Constrained Investor's income plan.

Before the DOL's Fiduciary Rule, Constrained Investor was a significant advance in retirement income planning. Now, it is a monumentally important answer for agents to operate safely as ERISA investment advice fiduciaries. Read more below.

About Constrained Investor

The Constrained Investor Evaluator

Constrained Investor Income Planning Profiler

In the dynamic landscape of income planning, the stakes are high. Yet, a considerable portion of the financial advisor community persists in adopting a deficient income-generation methodology. The repercussions of unsustainable market conditions, combined with unprecedented fiscal stimulus, have led to inflation, a declining stock market, rising interest rates, and heightened economic uncertainty. This article explores the shortcomings of the prevalent market-based approach to income distribution planning and introduces an alternative paradigm known as Constrained Investor, aiming to revolutionize retirement income planning.

The Pitfalls of Market-Centric Approaches

Traditional investment advisors often advocate for a market-based approach to income distribution planning, emphasizing Asset Under Management (AUM) segmentation. While effective for asset accumulation, this method falls short during the decumulation phase, neglecting critical factors such as "flooring," risk mitigation, and longevity risk protection essential for retirement income planning.

Constrained Investor replaces AUM segmentation, or "wealth segments," with three, far more meaningful categories of investors who are nearing retirement or already retired. All investors will fit into one of the three categories: Underfunded Investors, Overfunded Investors or Constrained Investors.

Introducing the Constrained Investor Paradigm

Constrained Investor challenges the conventional AUM segmentation, categorizing investors nearing or in retirement into three meaningful groups: Underfunded Investors, Overfunded Investors, and Constrained Investors. This paradigm shift expands the assessment of client needs by examining the crucial relationship between investable assets and the "must-have" monthly income, fostering a more comprehensive understanding of retirement preparedness.

Changing the Income Planning Equation

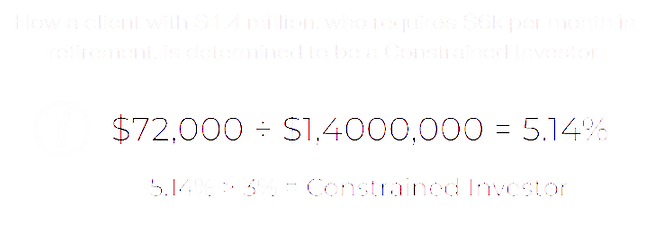

Advisors are sometimes surprised at how much money some Constrained Investors have accumulated- $10 million, or more. With an Assets-to-Income Ratio of 5.4%, a client with AUM of $20 million- who requires an income of $90,000/month- is very much a Constrained Investor. To determine if a client is Constrained, we use the Income-to-Assets Ratio. If the resulting percentage is 3%, or more, the client is a Constrained Investor.

Constrained Investor redefines income planning by prioritizing risk mitigation for those with limited margin for investment losses. By incorporating safe monthly paychecks and guaranteed lifetime income, this approach alters investor behavior dynamics, allowing retirees to remain invested in risk assets through various market conditions.

Addressing the Income Gap

The focus shifts from the total amount saved to the relationship between savings and the income required for a minimally acceptable lifestyle. The Income-to-Assets Ratio becomes a key metric, identifying Constrained Investors as those with a percentage of 3% or more. Surprisingly, even clients with substantial AUM, such as $20 million, may fall into the Constrained Investor category, emphasizing the importance of understanding this nuanced approach.

A Call for Annuities in Retirement Planning

The article stresses the significance of recommending lifetime guaranteed income, particularly through annuities, to Constrained Investors. Criticizing the "Wall Street" Approach and the widely used Systematic Withdrawal Plan, the author contends that failure to recommend annuities could breach the fiduciary duty of Registered Investment Advisors (RIAs), underscoring the importance of securing clients against longevity risk.

Overlooking "Boomer" Women: A Critical Oversight

The discussion expands to address the failure of the traditional Wall Street Approach in incorporating lifetime income annuities, leaving many "boomer" women vulnerable to longevity risk. Research suggests that the unique preferences and priorities of women in retirement planning are often overlooked by market-centric approaches. Recognizing this disparity creates a significant opportunity for advisors to cater specifically to women's needs, potentially avoiding the loss of clients and capitalizing on a massive market share.

Conclusion

In conclusion, the Constrained Investor paradigm offers a more holistic and personalized approach to retirement income planning, emphasizing risk mitigation and longevity protection. Financial advisors must adapt to these changing dynamics, especially in addressing the distinct concerns of "boomer" women, to ensure a secure and fulfilling retirement for their clients.

Contact David

978-375-3400

.jpg)